Wall Street’s $128 billion private credit exposure is starting to look harder to contain

JPMorgan Chase CEO Jamie Dimon told analysts in April that the roughly $1.8 trillion private credit market doesn't pose a systemic risk. “You have to have very large losses in private credit before, at least it looks...

Bitcoin 1 Minute

Here is the latest from the digital-asset markets: JPMorgan Chase CEO Jamie Dimon told analysts in April that the roughly $1. 8 trillion private credit market doesn't pose a systemic risk. “You have to have very large losses in private credit before, at least it looks like, banks are going to get hit,” he said.

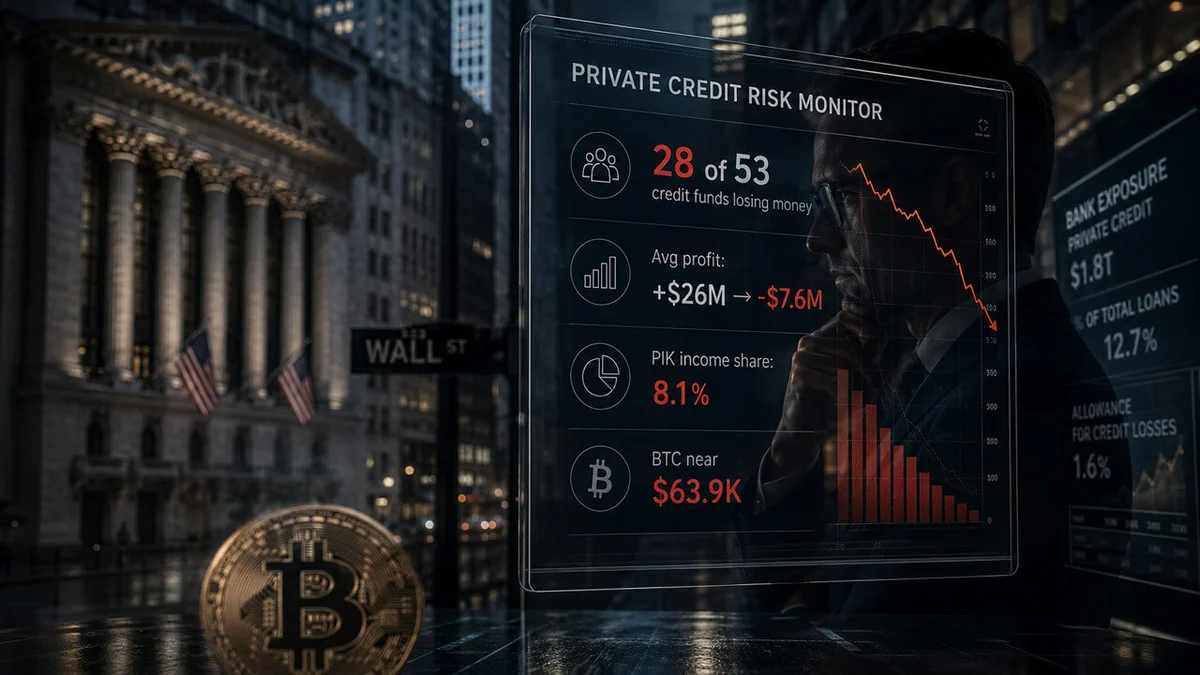

He made that comment the same week executives at Citigroup, Bank of America, and Wells Fargo used nearly identical language to describe their own exposures as “comfortable. ” But a analysis of 53 publicly traded business development companies found that 28 had swung into the red during the first quarter of 2026. Average profit collapsed from positive $26 million a year earlier to negative $7.

Market Dynamics

The visible losses may be only the first layer of a funding structure that runs from stressed borrowers through leveraged lenders and back onto the balance sheets of the very banks insisting the danger is contained. Related Reading From Jamie Dimon to Donald Trump: Why everyone eventually understands Bitcoin What was once met with skepticism and doubt is now universally accepted at the highest level. Despite the resistance, eventually everyone understands Bitcoin.

Sep 6, 2025 Christina Comben BDC losses, phantom income, and the leverage banks don't see Business-development companies, or BDCs, are essentially publicly traded private credit funds. They lend money to mid-sized companies that can't easily get bank loans, and they pass most of their income back to shareholders as dividends. conducted the analysis with S&P Global Market Intelligence, examining standardized financials across 53 of them.

Twenty-eight were loss-making in the first quarter of 2026, up from just 12 one year earlier. Average profit fell to negative $7. 6 million from positive $26 million, a shift driven largely by loan markdowns and rising borrowing costs.

Market Impact

BDCs often emphasize net investment income in their own reporting, but the standardized approach captures debt expenses and changes in loan valuations that managers sometimes obscure beneath adjusted metrics. It's a gap that can mislead anyone relying on headline figures alone. When a BDC says it's earning steady income, it might not be counting the loans that are steadily losing value on its books.

Not all of that income was cash. Payment-in-kind, or PIK, is a way borrowers can add interest to their debt balances rather than pay it in cash. It preserves liquidity today while increasing the amount owed tomorrow.

PIK accounted for an average of 8. 1% of BDC interest and dividend income in 2025, roughly twice its pre-2020 share. That doesn't prove losses are imminent, but it weakens the comfort supplied by headline income figures.

Crypto markets are watching this development closely as investors weigh its potential impact on prices.